Brian Baker, Drew Hyatt, Brian Klepper

5 Minute Read

A Macro View

Recently RAND released the fifth in a series of employer focused reports: “Prices Paid to Hospitals by Private Health Plans”, the fifth in a series of employer-led transparency reports, developed in conjunction with the Employers Forum of Indiana and funded by the Robert Wood Johnson Foundation. In this report, they focus on average prices paid for hospital services. According to CMS, in 2022, hospital spending accounted for 42% of total personal healthcare spending, making it a great subset of costs to study. But hospital services are not responsible for the majority of costs.

The report has terrific detail that informs discussions on hospital pricing and offers ideas for employers. But the hospital pricing report focus omits consideration for everything else, the 58% of spend.

Some of the report’s conclusions are obvious but difficult to achieve. For example, “…price transparency alone will not lead to changes if employers do not or cannot act upon price information.”

Others are not so apparent, like the fact that great price variation exists within and across markets – In those discussions, the report points out median differences between Medicare and hospital inpatient and outpatient payments, comparing intensity-weighted price ratios rather than absolute price differences for specific services. This approach represents great effort attempting to help employers assess and leverage value. But it misses the real leverage point. The absolute price is what is paid for each claim, not intensity-weighted rates.

This year US employers will provide more than 150 million Americans with fully insured or self-insured benefit plans that cost $1.3 trillion, More than one-third of that, $486 billion, will be for hospital related care, which the report focuses on. What is omitted is the remaining two-thirds of “routine” non-hospital related spend. As a practical matter, the new fiduciaries under the CAA, the employers, need insights to the two-thirds of spend in order to understand how the numbers play out locally and then impact costs.

Pricing-Variability Legacy

In 2011-2012, Baker led a series of peer-reviewed, published research projects highlighted the payment disparities between hospital-based and freestanding outpatient imaging services. 6.9 million exams over four years were sampled, focusing on the facility fee or non-physician portion of the service, including Government (Medicare, Medicaid) payment amounts. The blended national cost disparity was 241%. For the same service, the study proved it would cost 2.41x more on average to get your imaging exam done at a hospital or hospital-owned clinic compared to a stand-alone outpatient clinic. This 2.41x perspective was a solid benchmark of historical price variability for the CAA study described below.

CAA Delivers Revelations

Studying the public health plan pricing files now available thanks to the CAA is an undertaking. They are presented in a nested format difficult to decompile and unfriendly to simple navigation or viewing and can, in some cases, be hundreds of gigabytes in size. A single self-insured employer’s health plan pricing data can consist of as many as 60 of these files. The employer we studied for this article is a one location employer with a BCBS plan and 800 employees in one market within one of the top ten ranked cities in the US for economic growth, jobs, quality of life etcetera. The almost 60 decompiled files represented 200 million lines of providers, prices, codes and so on.

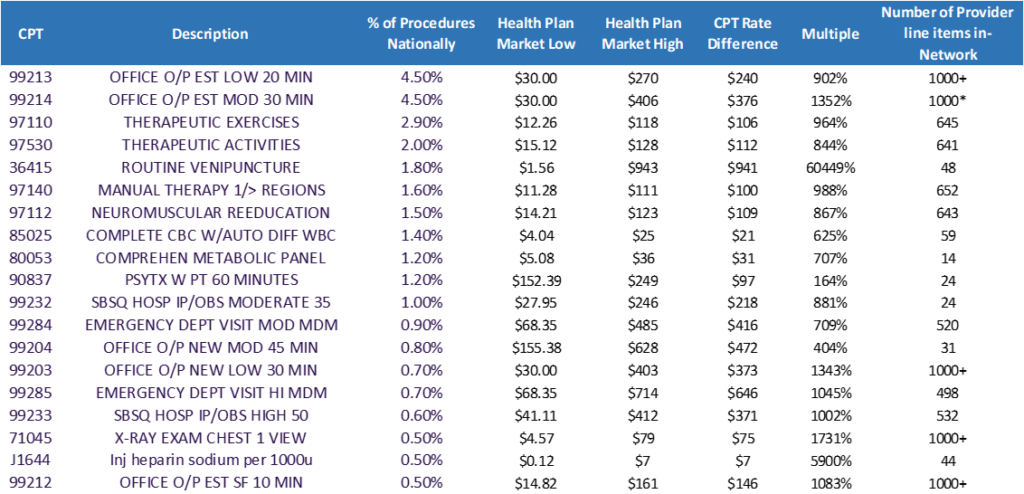

Modeling ideas in an effort to support the self-insured employer, we decided to use the trusty 80/20 rule. So we chose the top 20 CPT codes for all claims across the U.S. The top ten of those 20 CPT codes together represent over 22 percent of all codes within claims. Two of those CPT codes, 99213 and 99214, delineating office visits, share the #1 spot at a whopping 4.5 percent of all claims.

Looking at these ten CPT codes, we analyzed the lowest and highest negotiated rate within the plan as well as the total number of providers listed for the CPT code within the plan to understand the variability and scope of choice for a consumer. The results surprised us.

Over 60,000 Percent?

The CPT codes we studied here are not complex procedures. They are common and available in a wide variety of settings. They include things such as physical therapy, routine venipuncture, a complete CBC or metabolic lab test. We are not talking knee replacement surgeries or coronary artery bypass grafts (CABGs) here.

On average, more than 400 providers were available to deliver the services associated with each code. You want physician choice? You’ve got it!

The largest pricing variability between the lowest negotiated rate and highest rate within these ten codes was 60,449 percent. The lowest rate was $1.56 and the highest was $943. Is this an outlier?

The second largest price variability was for one of our #1 CPT codes and revealed 1,352 percent. Lowest cost is $30. Highest is $406. Another outlier? We don’t think so.

If we tossed out the 60,449 percent outlier, the average high-low price differential between the remaining nine codes was 823 percent – more than an 8x price differential across an average of 400 provider options for only 10 CPT codes representing about 20 percent of all codes in US claims.

The Solution

The Rand report’s undeniable conclusion is for employers to use their health plans’ data to renegotiate provider contracts. With deference to and much respect for the RAND team’s great work, we believe the transparency files data reveals a quicker path to healthcare spend reductions.

Employers that want to lower healthcare spending should find a tool that provides members with the pricing and provider choices that use the variability opportunity already in their plans. This solves several problems.

1. This information is required (among many other things) as part of a self-insured employers fiduciary duties within the CAA.

2. Providing personalized data in the context of “What is my portion of this cost going to be?”, allows members (and the employer) to interact with the data to make informed decisions prior to getting a service.

3. Providing data this way, employers can modify their plans with incentives that promote wise cost choices while not embarking on wholesale renegotiation efforts as a first step.

You can bet your members shop for things they need every day. Leveraging the information unveiled by the CAA can have an immediate impact. Providing your members a solution that tracks their healthcare journey and helps them cost compare is the first step. Then incentivize them and watch the average unit cost of your healthcare benefits drop.